IP Monetization 101: Unlocking a New Pocket of Hidden Value

1 October, 2020

To succeed in today’s marketplace, technology-driven companies must excel at identifying and adapting to new opportunities rapidly and efficiently. Yet many companies fail to spot new sources of “unexpected” revenue—sources that in some cases are hiding in plain sight. Non-core technology assets—where significant R&D investments were made or acquired—don’t call attention to themselves. What they can do is generate a significant one-time cash infusion if fully divested or a new recurring revenue stream if licensed.

Correctly identifying and valuing technology-related non-core assets within a larger strategic plan (as part of an M&A process, for example) demands a specific kind of sleuth. Corporate management is expected to be adept at creating, identifying, marketing, and monetizing core technologies and IP. But management doesn’t typically possess the experience required to identify dormant value in the form of non-core tech assets. Even if they do have the requisite experience, they often simply don’t have the bandwidth to execute a monetization project for non-core assets.

The good news is that there is a methodology for realizing value from these assets. Guided by an advisor who can identify non-core tech assets, accurately determine their market value and execute the transaction, companies can unlock unexpected competitive advantages.

WHAT ARE NON-CORE TECHNOLOGY ASSETS?

Non-core technology assets are essentially intangible assets that are superfluous to a company’s current products and market applications. In many cases, non-core assets can represent significant unrealized value. They accumulate as a result of several factors:

- IP developed under an R&D strategy that has since been shelved, even though “it worked.”

- Technologies and products that were acquired as part of a larger M&A transaction.

- Products based on solid R&D but with poor future strategic fit due to organizational changes.

There is a strong and growing market demand for developed technology assets. One company’s burning technology need could be sitting in another company’s basement as non-core technology. Rapid changes in the technology landscape are forcing many companies to innovate faster than their internal R&D systems allow or in areas where they have no expertise. This drives those companies to look for technologies that someone else has already developed, regardless of whether the original developer built a real business around it.

There is a strong and growing market demand for developed technology assets. One company’s burning technology need could be sitting in another company’s basement as non-core technology. Rapid changes in the technology landscape are forcing many companies to innovate faster than their internal R&D systems allow or in areas where they have no expertise. This drives those companies to look for technologies that someone else has already developed, regardless of whether the original developer built a real business around it.

Another helpful factor is the recent influx of capital from the private equity community and alternative investment funds seeking uncorrelated ROI, which technology investments offer—so the buyer of non-core technologies could be a financial investor, not just another operating company.

However, many businesses lack the staff bandwidth or expertise to separate core from non-core tech assets, identify potential buyers, and execute a transaction.

UNLOCKING BURIED TREASURE

M&A scenarios present the most opportunities and challenges when it comes to capitalizing on non-core assets. Sellers, for example, often presume their advisors will value core and non-core assets collectively as part of the M&A process. In reality, traditional financial advisors often overlook non-core technology that hasn’t already been successfully monetized, either as in-process R&D or obsolete products. Buyers, for their part, inherently regard all of a target company’s technology and IP as “priced into the deal” and aren’t prepared to pay separately for non-core tech assets if they are not already generating revenue. Presuming a business can identify these assets, monetizing them is another matter entirely. There are a variety of challenges, and it’s important to identify non-core technologies that are not suitable for monetizing:

- Non-core technology may require significant up-front capital expenditure to be made market-ready, which can reduce its attractiveness to a prospective buyer.

- A particular technology may have grown obsolete for that buyer.

- The technology development team may no longer be developing this particular non-core asset or may have moved on, hampering technology transfer and value to a buyer.

FOUR KEY QUESTIONS

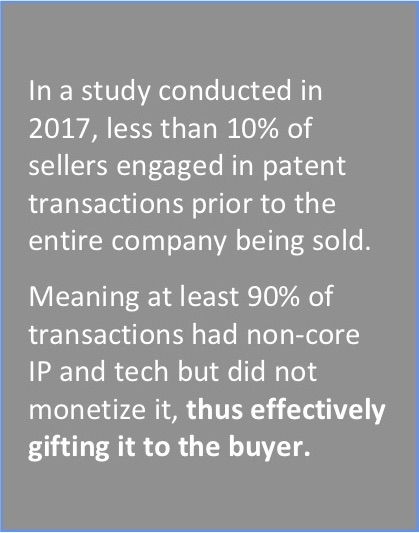

A Houlihan Lokey study conducted in 2017, based on its deal experience and technology M&A deal data from PricewaterhouseCoopers, examined 1,000 M&A transactions involving technology companies. Focusing on sellers who held both core and non-core patents prior to being acquired, we estimated how many sellers had engaged in patent transactions prior to the entire company being sold. It turned out to be less than 10%. In other words, at least 90% of the covered transactions had non-core IP but did not monetize it, thus effectively gifting it to the buyer.

A Houlihan Lokey study conducted in 2017, based on its deal experience and technology M&A deal data from PricewaterhouseCoopers, examined 1,000 M&A transactions involving technology companies. Focusing on sellers who held both core and non-core patents prior to being acquired, we estimated how many sellers had engaged in patent transactions prior to the entire company being sold. It turned out to be less than 10%. In other words, at least 90% of the covered transactions had non-core IP but did not monetize it, thus effectively gifting it to the buyer.

Testing the market viability of non-core technology starts with a preliminary internal test. Whether you’re a potential buyer or seller, here are four key questions to consider:

- Did the non-core technology asset result from serious R&D investment (i.e. greater than $10 million), including proof-of-concept and proof-of-market?

- Does the technology or product work reliably today and generate at least some EBITDA?

- What exactly renders it non-core—strategic fit, margins, markets?

- Can it be repurposed for other uses in other industries?

However, many businesses lack the staff bandwidth or expertise to separate core from non-core tech assets, identify potential buyers and execute a transaction.

THE BOARD PLAYS A KEY ROLE

The value of these non-core technology assets belongs to the shareholders of the seller. The board’s job in an M&A setting is to thoroughly review all of the pockets of value that exist in a company, before a transaction, to maximize value prior to and during a company sale. In order to do so, the board must be well informed enough to choose an appropriately experienced advisor.

Directors must ask questions such as:

- How extensive are the company’s non-core tech assets and what is the financial value when viewed within a variety of contexts?

- Is the value of these assets material to the overall size of the anticipated core M&A deal? Generally, “material” means more than 5% of the valuation; in practice, the bar is frequently set at 10% to 15%.

- If they pass the materiality test, what are all the strategic alternatives available to realize the value of non-core tech assets?

THE VALUE OF A TRUSTED KNOWLEDGEABLE ADVISOR

Developing strategic alternatives around non-core technology assets demands specialized knowledge. In addition to understanding buyside and sellside processes, an advisor must have demonstrated experience in technology product transactions—particularly non-core assets. This includes:

- Proven experience analyzing the quality of non-core assets, assessing market opportunity, and arriving at the right valuation.

- Ability to conduct a thorough, nuanced evaluation of existing licensing arrangements.

- A firm grasp of the interplay of IP rights and current customer obligations in the context of non-core assets.

- Capability to creatively repurpose the assets across industries and geographies, and find a broad range of interested potential buyers.

To learn more, watch the webinar recording now as Elvir Causevic, explores best practices in IP monetization strategies and the successful ways the Tech+IP Advisory Practice at Houlihan Lokey has applied an M&A-like process to patent monetization.